It’s fair to say most people like the idea of budgeting.

Being organized

Feeling secure

Knowing where your money’s going instead of wondering where it went

But when it comes to actually doing it?

That’s where the disconnect starts.

Because traditional budgeting doesn’t just track your money—it also tends to drain your energy.

The spreadsheets

The guilt

The feeling that if you mess up once, the whole thing unravels

No wonder it’s hard to stick with

But what if budgeting didn’t feel like budgeting?

What if it wasn’t color-coded?

Or didn’t involve combing through every transaction?

And what if it didn’t make you feel like you were failing every time you forgot to log a coffee?

Because here’s the thing most people won’t tell you:

The goal isn’t to follow a perfect budget

It’s to feel in control of your money

Without obsessing over every penny

That’s possible

And it doesn’t require a complete system overhaul

Start by noticing your money’s rhythm

Every income has a rhythm.

Every expense has one too.

You might not have it written down—but you already know the basics.

Rent hits on the 1st

Groceries fall on Saturdays

The auto-payment sneaks out mid-month

Budgeting doesn’t have to mean building something new from scratch

Sometimes it just means putting words to what’s already happening

Have you ever noticed you spend more when you feel scattered?

Or that your best months happen when you don’t think about money 24/7?

That’s a rhythm worth leaning into

Divide, don’t detail

Most people abandon budgeting because it asks too much.

Track everything

Categorize everything

Justify everything

That’s exhausting and feels like a lot of hard work

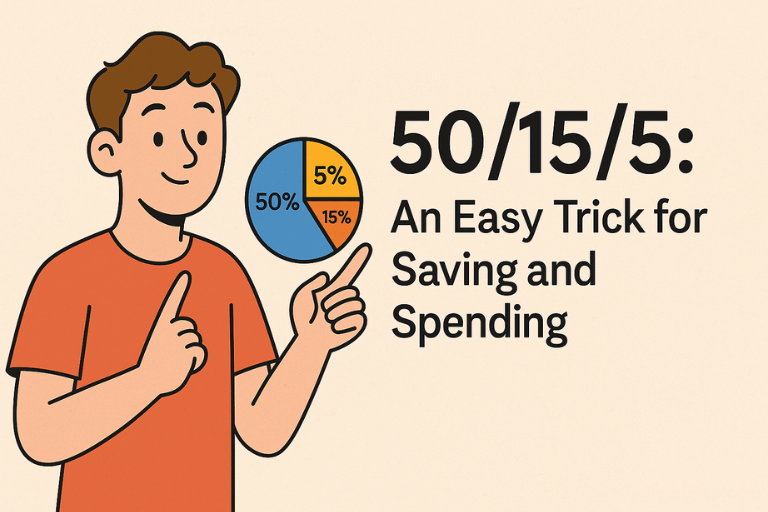

Instead, break your money into just a few mental buckets

Fixed: rent, bills, insurance

Flexible: groceries, gas, household

Fun: everything else

You don’t need 14 categories to be intentional

You just need boundaries that feel realistic

And when the lines are simple?

You’re more likely to actually follow them

Automate what annoys you

One reason budgeting feels like a chore is that it is a chore

So the less of it you have to do, the better

- Auto-pay bills

- Set recurring transfers to savings (even small ones)

- Use banking apps that categorize spending for you

It’s not about losing control

It’s about reducing friction

Because when things happen automatically, you’re free to focus on decisions—not details

Ever looked back on a month and thought,

“I didn’t even realize I was doing the right thing”?

That’s what automation gives you

Don’t make your system prettier than it is useful

This one sneaks in when you’re “motivated”

You download a new budgeting app

And efficiently start logging receipts

You color-code categories and plan no-spend days

And for a week? You feel amazing

Then life happens

You get busy

You miss a few entries

And suddenly, the whole thing collapses

People don’t quit budgeting because they’re bad with money

They quit because the system they built only worked when nothing else went wrong

Pause here for a second…

This might be the moment where you think:

“So basically, just do less?”

Kind of.

But not out of laziness

Out of strategy

Because if the system only works when your energy is high

It’s not a sustainable system

And sustainable systems are the only ones that stick

So the next time you want to “get back on track”—ask yourself:

Would this still work on my most tired day of the month?

If not, it needs to be simpler

Final thought

You don’t have to budget like an accountant to stay in control

You don’t need a binder

You don’t need a checklist

And you definitely don’t need to feel bad every time real life doesn’t match your projections

Budgeting doesn’t have to look like budgeting

It just has to work

Quietly

Consistently

In the background of your life

And when it does?

That’s when you know you’ve finally built something you’ll actually keep using

Note: This content is for entertainment purposes only and is not financial advice. Please consult a qualified financial advisor for guidance specific to your situation.