Ever wonder how your finances compare to everyone else’s?

You’re not alone

There’s something quietly comforting

and a little bit unsettling

about knowing where you stand

Are you ahead?

Falling behind?

Or just somewhere in the messy middle?

Looking at the numbers doesn’t solve anything

But it does give you perspective

And in today’s financial climate

a little clarity goes a long way

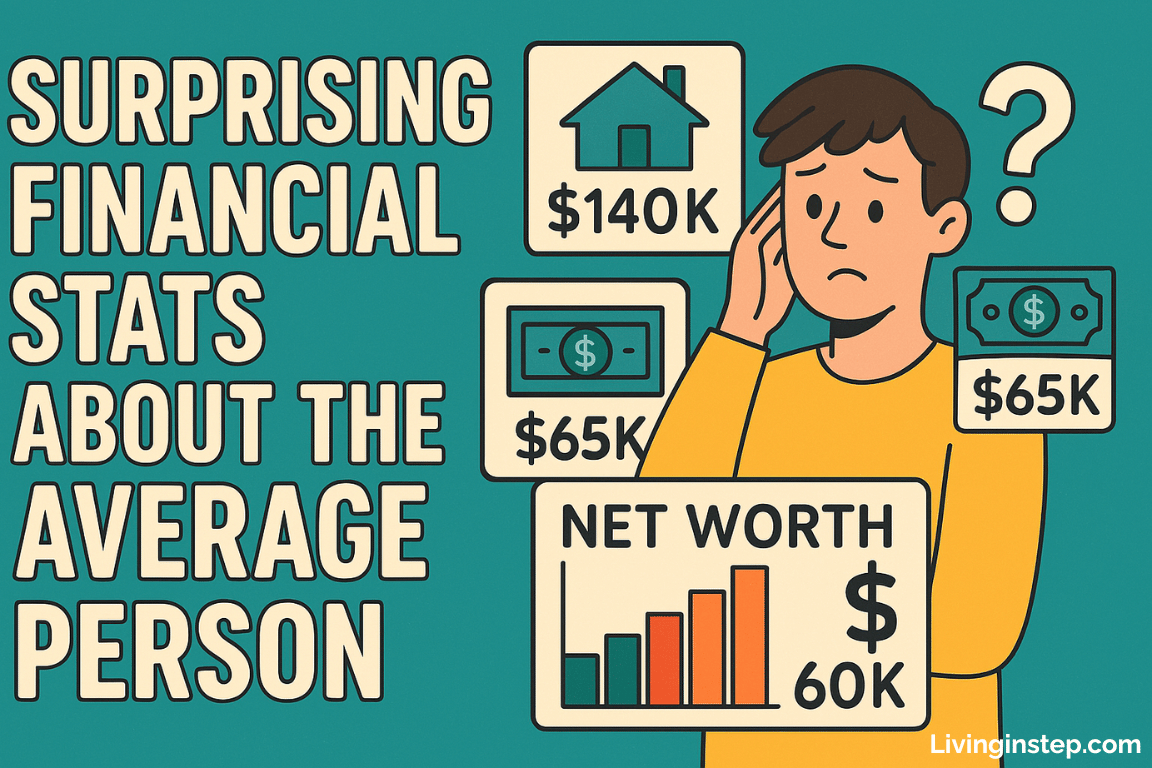

Median income in the U.S.

Let’s start with the basics: how much people actually make

According to the latest data from the U.S. Census Bureau:

- Median household income: $74,580 (2022)

- Median individual income: Roughly $40,000–$45,000

That means half of people earn less than that

Even in dual-income homes

So if you’re not pulling in six figures?

You’re not behind

You’re exactly where most people are

The average credit score

This one might surprise you

- Average FICO score in the U.S.: 717 (as of 2023)

That’s considered “good”

But the distribution tells a better story:

- Around 15% of Americans have scores below 600

- Roughly 23% are in the excellent (800+) range

Which means most people are sitting in the middle

Juggling bills

Carrying balances

Trying to keep things stable

How much people are saving for retirement

Here’s where things start to get uncomfortable

According to Vanguard’s 2023 report:

- Average 401(k) balance: $112,572

- Median balance: $27,376

And broken down by age:

- Under 25: ~$5,200

- 25–34: ~$30,000

- 35–44: ~$76,000

- 45–54: ~$142,000

- 55–64: ~$207,000

- 65+: ~$232,000

It’s not nothing

But it’s not enough to fully retire for most people

Which is why so many are planning to work longer

or rely heavily on Social Security

Social Security: What people can expect

The average monthly Social Security benefit (as of 2024):

- $1,907/month

That’s $22,884/year

For millions, it’s their main source of income after retirement

And it’s why even a modest nest egg

can make a major difference

Social Security isn’t designed to fully replace your income

It’s designed to supplement your savings

But for most, it’s the entire plan

Spending habits (and where the money goes)

The average U.S. household spends about $72,967 per year (BLS data, 2022)

Here’s where it goes:

- Housing: $24,298

- Transportation: $12,295

- Food: $9,343

- Personal insurance & pensions: $7,873

- Healthcare: $5,850

- Entertainment: $3,458

- Cash contributions (gifts/charity): $2,755

- Apparel: $1,945

- Education: $1,335

It adds up

And it shows why so many people live paycheck to paycheck

Even on a decent income

Net worth reality check

According to the Federal Reserve’s most recent Survey of Consumer Finances (2022):

- Median net worth in the U.S.: $192,900

- Average net worth: $1.06 million (skewed by the ultra-wealthy)

By age, median net worth looks more like this:

- Under 35: ~$13,900

- 35–44: ~$91,300

- 45–54: ~$168,600

- 55–64: ~$212,500

- 65–74: ~$266,400

The lesson?

Most people aren’t wealthy

They’re just doing their best to stay above water

and save when they can

Debt is everywhere

Here’s the breakdown of average U.S. household debt (2023, Experian):

- Credit card debt: $6,501

- Auto loans: $23,792

- Student loans: $28,950

- Mortgage debt: $236,443

- Total debt balance: $101,915 (per adult consumer)

Debt is normal

But that doesn’t mean it’s comfortable

And it definitely doesn’t mean people are thriving

So how do you actually compare?

You might be ahead

You might be right in the middle

Or you might be trying to catch up

But either way—

you’re not alone

These numbers aren’t meant to shame or impress

They’re meant to give you a sense of where things really stand

Because no one talks about this stuff

Everyone assumes everyone else is doing better

But the truth?

Most people are quietly figuring it out

Just like you

Note: This content is for entertainment purposes only and is not financial advice. Please consult a qualified financial advisor for guidance specific to your situation.